What Is Bank Fraud? How to Recognize It, Avoid It and Report It

What Is Bank Fraud? How to Recognize It, Avoid It and Report It How to Open a Bank Account for a Minor

How to Open a Bank Account for a Minor How to Balance a Checkbook

How to Balance a Checkbook Retirement Savings: How Much Should I Save Each Month?

Retirement Savings: How Much Should I Save Each Month?How to Cash In Savings Bonds

If you have recently stumbled upon savings bonds you were gifted as a child or some of your bonds are close to their maturity date, you may be wondering how to cash them in. Luckily, you can redeem savings bonds in multiple ways and choose the method that works best for you. Here’s how to cash in your savings bonds — and put a little extra money in your pocket.

What are savings bonds?

Savings bonds are an investment vehicle backed by the U.S. government. These bonds are available to buy in values ranging from $25 to $5,000, and you’ll earn interest on the amount of the bond over time.

You can choose from a few types of savings bonds, and each one earns interest a little differently. Here’s what you need to know about each one:

- Series E/EE bond: earns interest at a fixed rate over a term of 30 years, or until you cash it in, if you choose to do so before the term is up

- Series I bond: combines a fixed interest rate with an inflation rate over a term of 30 years (the inflation rate resets every six months, while the fixed rate doesn’t change)

- Series H/HH bond: These bonds were sold from 1980 through 2004 and are now discontinued. They were sold at face value, and then investors received direct deposit interest payments into their checking or savings accounts over a period of 20 years.

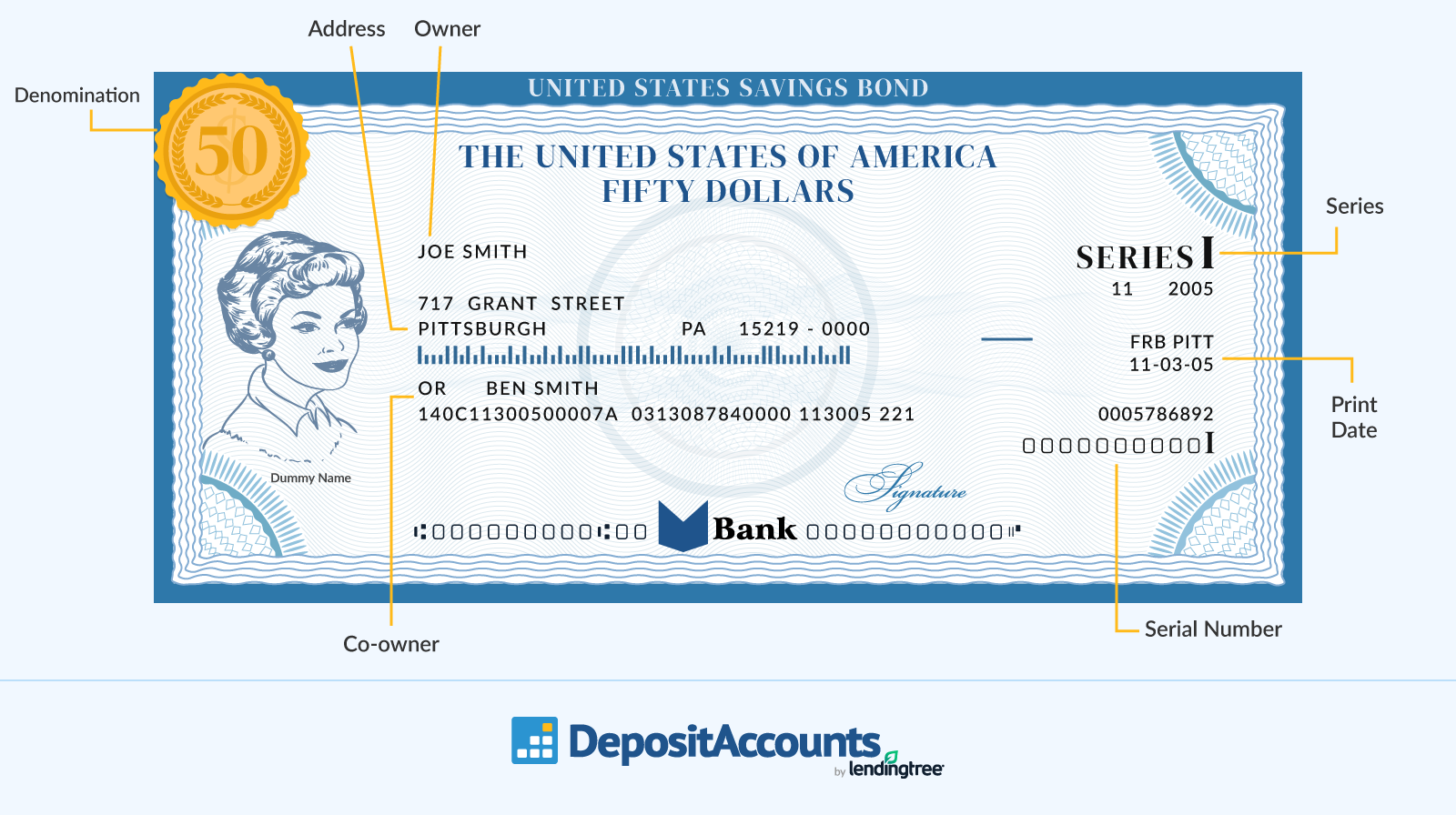

No matter what type of savings bond you have, it will contain the same important identifying information, which you’ll need to know when you’re ready to redeem the bond.

3 ways to cash in savings bonds

When you’re ready to cash in your savings bonds, there are three ways you can do it:

1. Create an online TreasuryDirect account

Electronic Series EE and I savings bonds can be redeemed on the TreasuryDirect website. To do this, you’ll need to create an account by providing your Social Security number, address, bank account information and email address.

Once your account is set up, you can redeem up to 50 bonds per transaction as long as you have held the bonds for at least a year before redeeming them. You’ll be able to choose whether you want to redeem part or all of each bond.

However, you must cash in at least $25 per transaction. If you redeem part of a bond, you’ll only receive an interest payment on the portion you redeem and must leave at least $25 in your account.

After you’ve confirmed your selections, the total amount of your redemption will be transferred into your linked bank account within two business days.

2. Mail in FS Form 1522

Alternatively, if you have paper bonds, you can cash them in by filling out FS Form 1522 and mailing it back to the Treasury Department.

To complete the form, you’ll need to be the owner or co-owner of any bonds you plan to redeem. You’ll also need to redeem them in full; you can’t request a partial redemption, as you can with an electronic bond.

When filling out the form, you’ll be asked to provide:

- Your name as it appears on the savings bond

- The issue date and serial number for any bonds being redeemed

- Your Social Security number or employee identification number

- Your bank account information

- A signature and proof of identification

If the total amount of the bonds you’re redeeming is less than $1,000, you can simply sign the form and include a copy of your government-issued ID (driver’s license, state ID, passport or military ID) with the rest of your paperwork. However, if the amount is greater than $1,000, you’ll need a certified signature. That means you’ll have to go to your bank or credit union and sign the document in front of a notary.

Once the form is filled out, you can mail it, along with the bonds themselves, to the address below:

Treasury Retail Securities Services

P.O. Box 9150

Minneapolis, MN 55480-9150

3. Visit your bank or credit union

You can also cash in savings bonds by visiting your bank or credit union. In this case, you’ll need to bring supplemental documentation with you in addition to the paper savings bond. It’s a good idea to call the bank or credit union ahead of time to ask about its requirements.

Typically, if you’re listed as the owner or beneficiary of the bond, you’ll simply need to bring proof of identification with you, such as a driver’s license or passport. However, if there are special circumstances, you may need to bring additional paperwork. For example, if the owner of the bond has died, you may be asked to provide a valid death certificate.

When is the right time to cash in a savings bond?

At a minimum, you’ll need to wait a year before redeeming your savings bonds. Also, if you redeem a Series EE or I bond within the first five years it is held, you’ll face a penalty worth three months of interest. After that five-year period, you can redeem savings bonds whenever you see fit.

Note that all savings bonds have maturity dates, which is when they stop earning interest. Once you hit that point, electronic bonds will be automatically redeemed. But you’ll have to remember to cash in paper bonds.

Here are the maturity dates to keep in mind:

- Series EE and I bonds: 30 years

- Series H and HH: 20 years

How much are my savings bonds worth?

Figuring out how much your savings bonds are worth is not hard. However, the method you use will depend on whether you have paper savings bonds or electronic ones. Here’s what to do:

Paper bonds

You can determine the value of any paper bonds you own by using the savings bond calculator provided by TreasuryDirect. Enter the series, denomination, issue number and serial number for each bond.

Electronic bonds

Meanwhile, you can see the value of any electronic Series I and EE bond by logging in to your account on the TreasuryDirect website. Once you’re logged in, simply navigate to the “Current Holdings” tab to see the value of any savings bonds you own.