5 Easiest Bank Accounts to Open Online

5 Easiest Bank Accounts to Open Online What Is Bank Fraud? How to Recognize It, Avoid It and Report It

What Is Bank Fraud? How to Recognize It, Avoid It and Report It How to Open a Bank Account for a Minor

How to Open a Bank Account for a Minor How to Balance a Checkbook

How to Balance a CheckbookIs Your Bank Healthy? Use Our New Bank Health Ratings Page

Over the past few months, we've made an enhancement to our Bank Health Ratings page. In addition to making it easy to evaluate the financial health of your bank or credit union, the new Bank Health Ratings page provides an overview of the financial health topic. The page shows how the financial health of banks has improved since the financial crisis, and it offers insights about the chance of a financially unhealthy bank failing. In addition, it describes the consequences that an unhealthy or failing bank can have on you.

You can access the Bank Health Ratings page from any page at DepositAccounts.com. Just select the "Banks" drop-down menu in the top navigation bar, and select the "Bank Health Ratings" link. Below is a snapshot of a piece of the DepositAccounts.com home page showing how to select the "Bank Health Ratings" page.

Interactive Slideshow

The first change you’ll notice in the Bank Health Ratings page is a multimedia slideshow which provides an overview of the financial health of the banking industry. The slideshow graphs show how the number of financially unhealthy banks have changed in the last eight years and how this correlates with the number of bank failures.

The banking industry is dominated by four "too big to fail" banks, and a failure at any one of these banks would impact the entire economy. As can be seen in the fourth slide, the "too big to fail" banks have grown larger since the financial crisis of 2008. However, their overall financial health has improved.

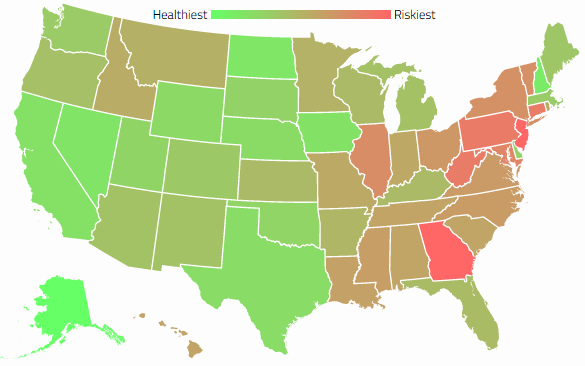

The last slide in the slideshow is an interactive map of the U.S. that ranks the states based on the financial health of the banks. The states with lighter green are the healthiest states, and those with lighter red are the riskiest states. To see the list of the healthiest and riskiest banks for each state, just click on the state in the map with the left mouse button. A pop-up box will display the health ranking of the state and include two links that point to the lists of the healthiest and riskiest banks in that state.

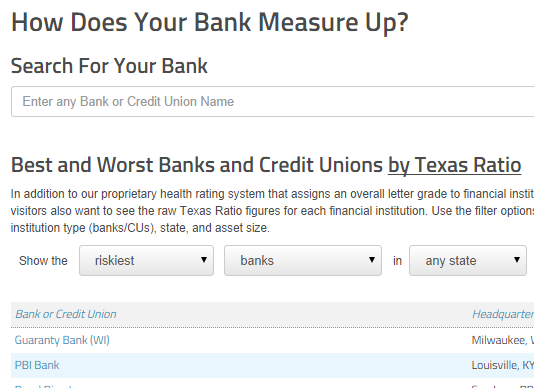

Learning About the Health of Your Bank

The lists of the healthiest and riskiest banks are actually an interactive table that allows you to filter the results based on institution type (bank or credit union), the state, and asset size. The banks and credit unions are ranked based on the Texas Ratio, which is a standard measure of a bank's credit troubles. Higher Texas Ratios indicate more severe credit troubles.

The Texas Ratio is one component of the proprietary formula used by DepositAccounts.com to assess the financial health of a bank or credit union. The components are combined into a letter grade in which an A+ indicates the best score and an F indicates the worst score. You can read more details about the Texas Ratio and the other components of the formula in the Bank Health Ratings page in the section right above the Texas Ratio table.

To find the Texas Ratio and the health grade of any federally insured bank or credit union, use the search box located just above the Texas Ratio table. When you find your bank or credit union, you’ll be taken to our hub page for that institution. One of the sections of this hub page covers the financial health. Each quarter we update the health grades based on new financial information released by the FDIC and NCUA.

Why the Health of Your Bank is Important

Finally, why should you care about the financial health of your bank or credit union? It might not seem important if your deposits always stay under the standard insured limits. However, there are several reasons to be concerned about the financial health of your bank or credit union. These reasons are listed in the Bank Health Ratings page right under the slideshow. One of the most interesting reasons is that it could affect your deposit rates. If the FDIC categorizes the bank less than well capitalized, the bank may be forced to keep its rates under FDIC rate caps. This has caused several banks to make substantial rate cuts to their reward checking accounts.